The Efficient Market Hypothesis (EMH), proposed by Eugene Fama in 1970, has long been regarded as a foundational theory in finance. It suggests that financial markets are „informationally efficient,“ with stock prices fully reflecting all available information. According to the EMH, only new information can influence the movement of stocks, rendering past movements irrelevant and unpredictable. However, in recent years, alternative theories such as the Fractal Market Hypothesis (FMH) have emerged, challenging the assumptions and limitations of the EMH. In this article, we will delve into the pros and cons of both hypotheses and explore the potential of the FMH to improve monetary policies and boost the economy.

Efficient Market Hypothesis (EMH):

The EMH posits that stock markets have no long-term memory and follow a random walk pattern. It suggests that beating the stock market in the long term is impossible, except for those who possess inside information or are willing to take higher risks. The EMH has been influential in shaping financial theory, with implications for investment strategies and models such as the Black-Scholes model, which is a foundational method to evaluate prices of options. However, critics argue that the EMH is not well-supported by empirical data and fails to account for certain market anomalies.

Pros and Cons of the EMH:

The EMH offers a straightforward and intuitive framework for understanding market behavior. It emphasizes the importance of quickly incorporating new information into stock prices, preventing individuals from consistently outperforming the market. Moreover, the EMH discourages insider trading and promotes market efficiency. However, critics argue that the EMH is not entirely supported by empirical evidence, as there have been instances where certain investors, like Warren Buffett, have consistently outperformed the market. Additionally, the EMH’s assumption of perfect market efficiency overlooks behavioral biases and market anomalies that can lead to mispricing and inefficiencies.

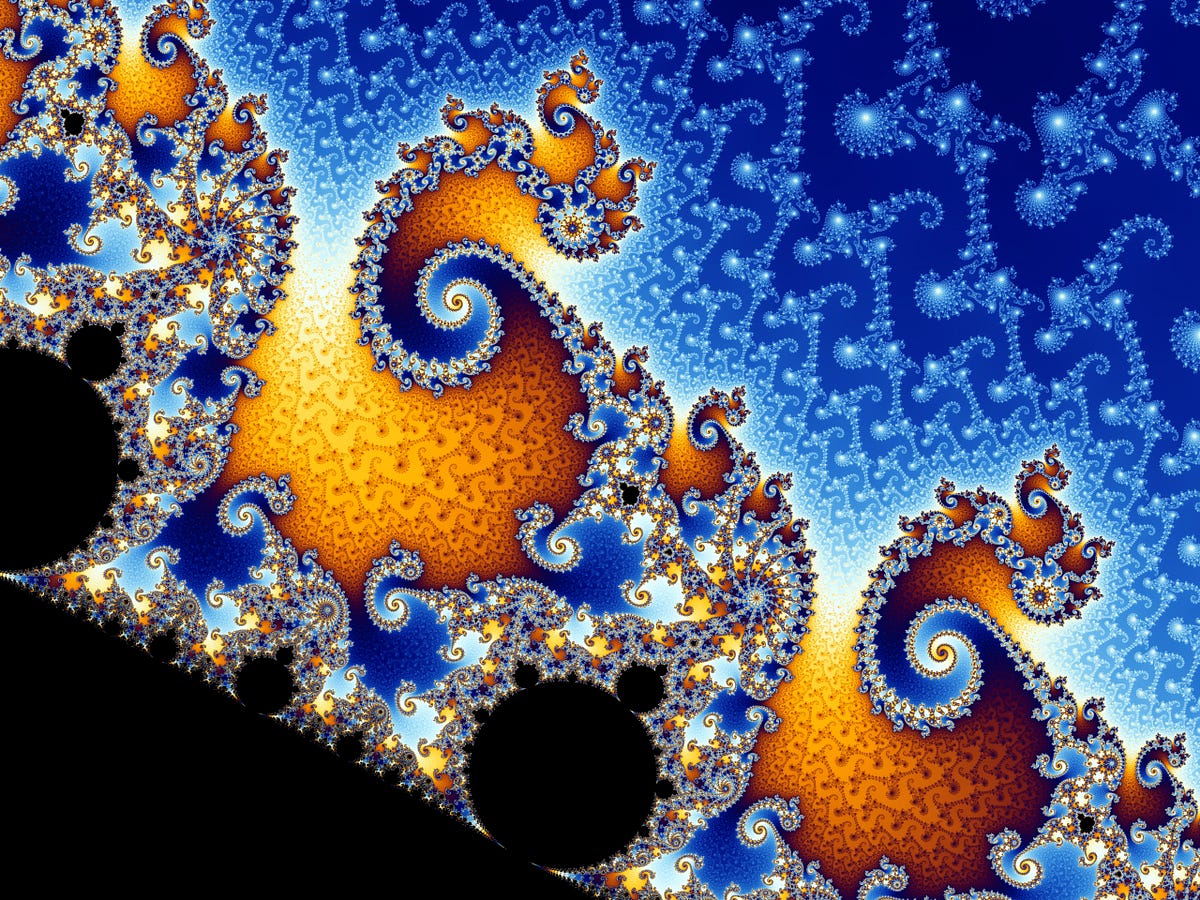

Fractal Market Hypothesis (FMH) as an Alternative:

The FMH challenges the EMH by suggesting that financial markets exhibit self-similarity, meaning that similar patterns occur at different time scales. Drawing inspiration from fractal geometry, the FMH proposes that market behavior can be better understood by accounting for the interactions of agents with different time horizons and interpretations of information. This alternative theory offers a more nuanced perspective on market dynamics than the EMH’s assumption of market efficiency.

Potential Benefits of the FMH:

The FMH has important implications for monetary policies and the overall economy. Fractal structures in market prices, as observed in the FMH, often indicate stability. Understanding the mechanics that generate fractal structures can enable policymakers to formulate measures that foster stable markets and incentivize interactions between agents with different time horizons. Moreover, the FMH may help explain and guide the regulation of high-frequency trading activities, reducing the occurrence of „flash crashes“ and improving market stability.

Conclusion:

While the EMH has been a fundamental theory in finance, the emergence of the FMH challenges its assumptions and limitations. The FMH offers a more nuanced understanding of market dynamics, emphasizing self-similarity and the impact of information and liquidity. Although the FMH is still in its early stages of development, it holds significant potential for improving monetary policies and enhancing overall market efficiency. As further research and empirical evidence accumulate, policymakers and market participants should remain open to alternative theories like the FMH to gain a deeper understanding of the complex nature of financial markets.

Editor: Tarik Asaad

Sources:

Fama, E. F. (1970). Efficient capital markets: A review of theory and empirical work. The Journal of Finance, 25(2), 383-417.

Peters, E. E. (1991). Chaos

Mandelbrot, B.B. & Hudson, R. L. (2008). The (mis)behaviour of markets: A Fractal View of Risk, Ruin and Reward

Mandelbrot, B.B. (1997). Fractals and Scaling in Finance: Discontinuity, Concentration, Risk

Anderson, N. & Noss, J. (2013). The Fractal Market Hypothesis and its implication for the stability of financial markets

Sinha, S., Chatterjee, A., Chakraborti, A., Chakrabarti, B. K. (2011). Econophysics: An Introduction

No Comments